Executive Summary

The Southeastern U.S. exhibits robust long-term multifamily demand that we believe will support sustainable rent growth and provide StoneRiver opportunities to identify compelling investments and create value for our investors. In this paper, we discuss the following economic and demographic factors that drive multifamily demand in the Southeast:

- Employment and wage growth

- Population growth, especially among young adults

- Household formation

- The cost savings and other advantages of renting compared to homeownership

We also show that despite the recent surge in new multifamily supply, demand remains solid in our target markets, which include Alabama, Florida, Georgia, Kentucky, North Carolina, South Carolina, Tennessee, Texas, and Virginia. Lastly, we highlight certain MSAs that we find favorable and unfavorable from a demand perspective.

This paper continues the analysis featured in our April 2024 white paper regarding supply, wherein we analyzed multifamily housing data across our geographic footprint, focusing on new supply, absorption, projected construction starts, population growth, and rent trends in key markets. In that paper, we concluded that the multifamily supply wave is a short-term dynamic that may create attractive investment opportunities in certain Southeastern markets.

StoneRiver’s data-driven approach to analyzing markets and submarkets within the Southeast allows our Investments Team to focus on the most promising areas and gives them an advantage in sourcing investment opportunities in a competitive market.

The Southeast’s Strong Job Markets Bolster Multifamily Demand

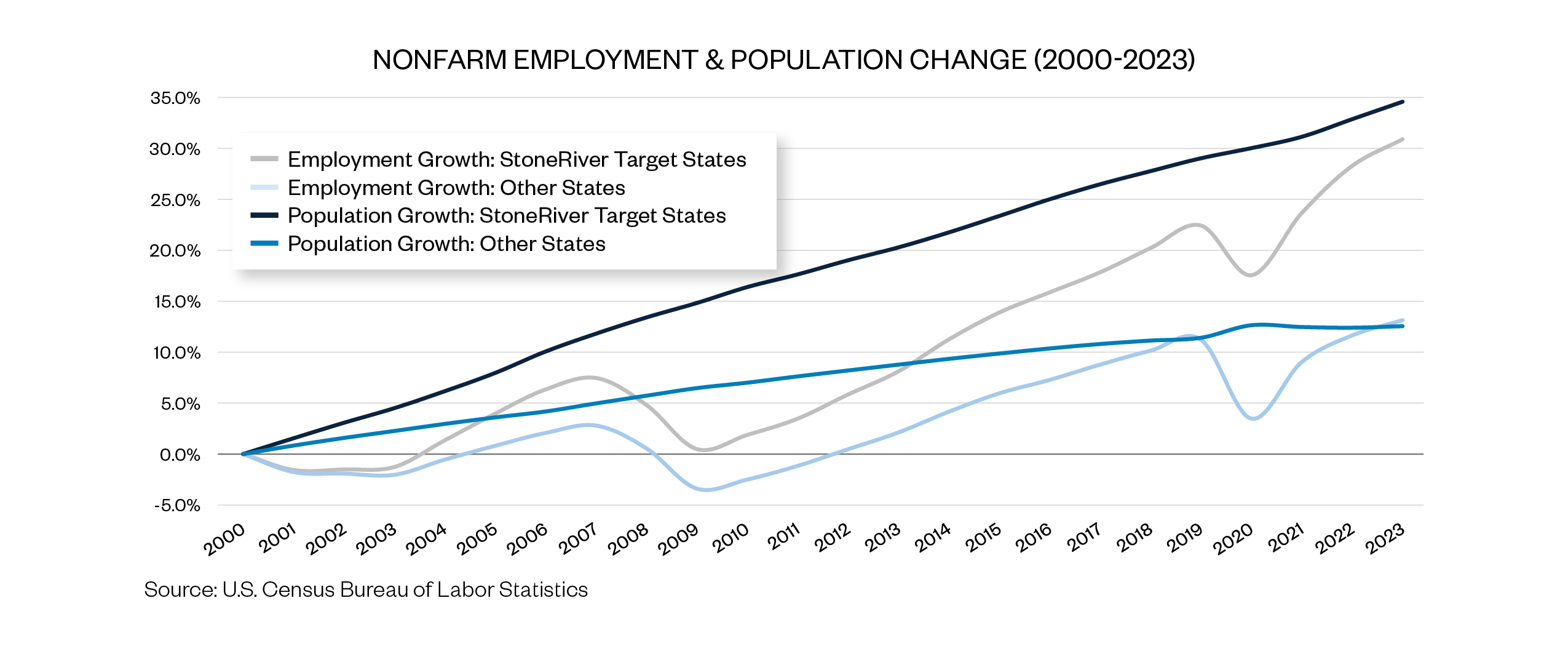

The Southeast features robust and diverse employment opportunities and impressive job growth. The region benefits from corporate relocations and the opening or expansion of large-scale service and manufacturing facilities due to its pro-business climate that provides a qualified labor force, tax credits and other business incentives, good infrastructure, and a favorable cost of doing business. Employment growth in our nine target states represented 47% of total job growth in the U.S. between 2000 and 2023. This impressive job growth has attracted strong inbound migration to the region. As shown below, job growth and population growth in our target markets have significantly outpaced that in other states since 2000.

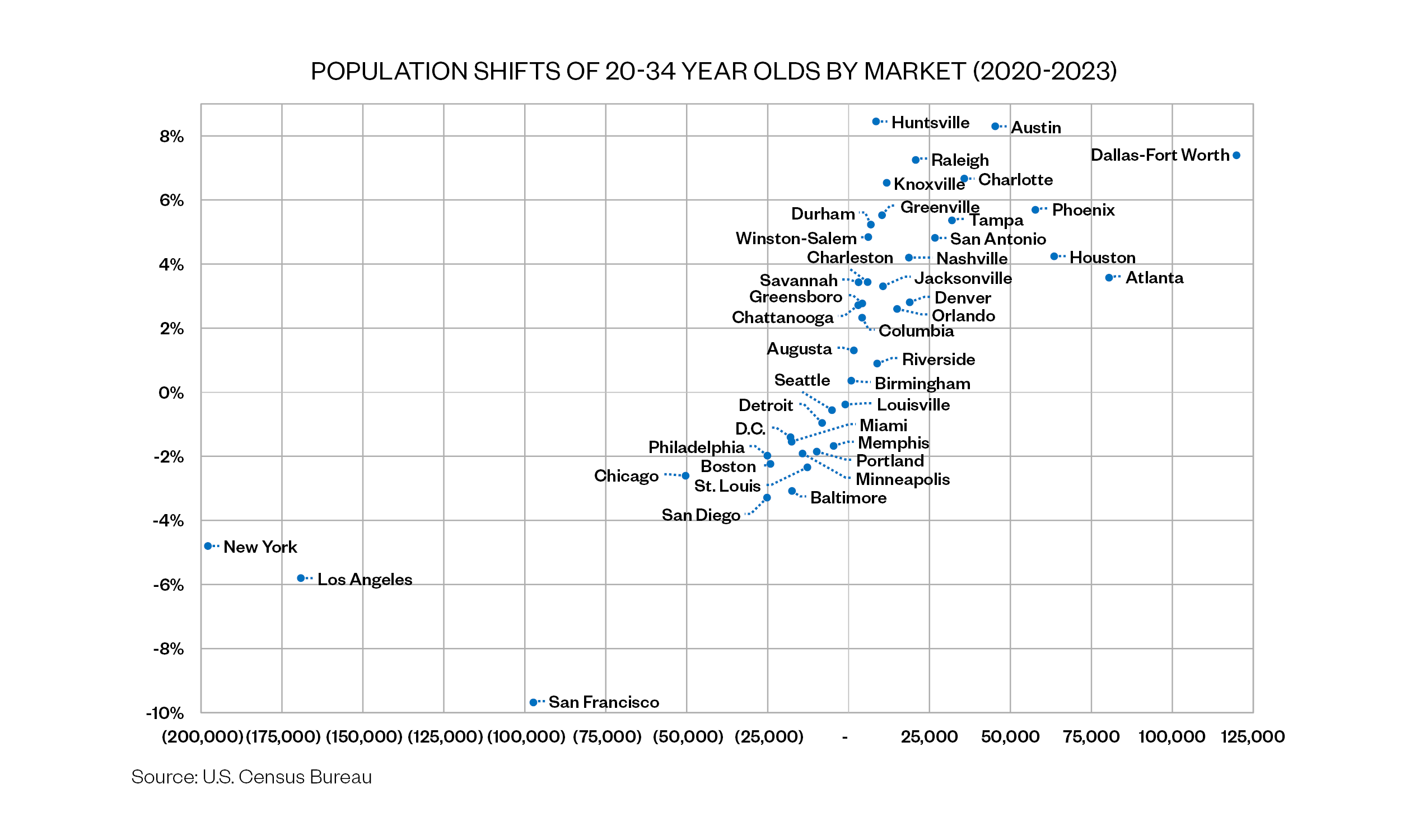

Population growth in the Southeast is particularly strong among young adults, who compose a large share of the renter population and are more likely to rent than own. The graphic on the next page includes StoneRiver’s Key MSAs¹ as well as any other MSA in the top 25 in the U.S. by population and shows that many Southeastern cities have attracted an impressive increase of 20-34-year-olds, while many major cities outside the Southeast saw a large decline.

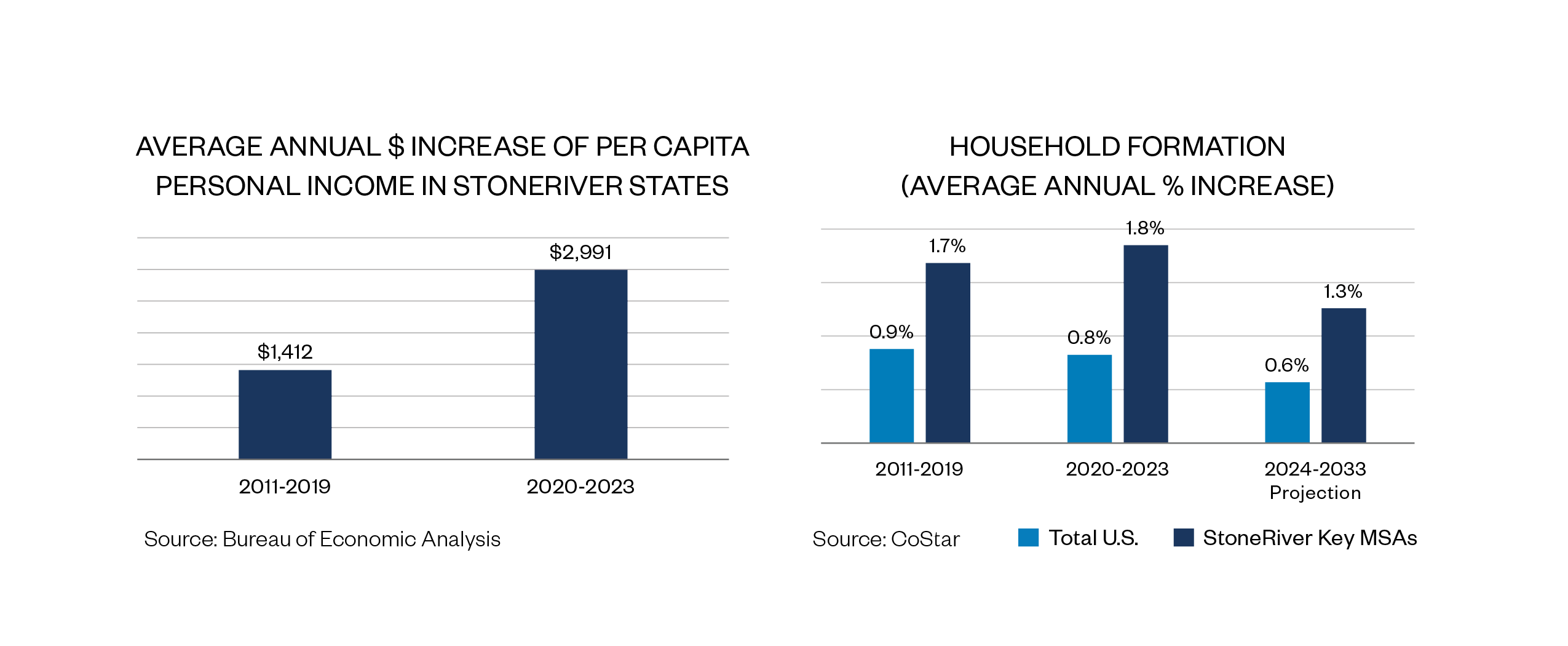

In addition to new jobs, wage growth in the Southeast has accelerated in recent years compared to historical levels. Wage growth spurs household formation by allowing people to move away from their parents or decouple from roommates. In fact, household formation in StoneRiver’s target markets far outpaces the national average and is projected to continue doing so. Despite this wage growth, the home price-to-income ratio reached an all-time high in 2022, and, as discussed below, the cost of homeownership far surpasses the cost to rent. Therefore, this wage growth and accompanying household formation should boost demand for apartments.

The Cost of Homeownership Fuels Multifamily Demand

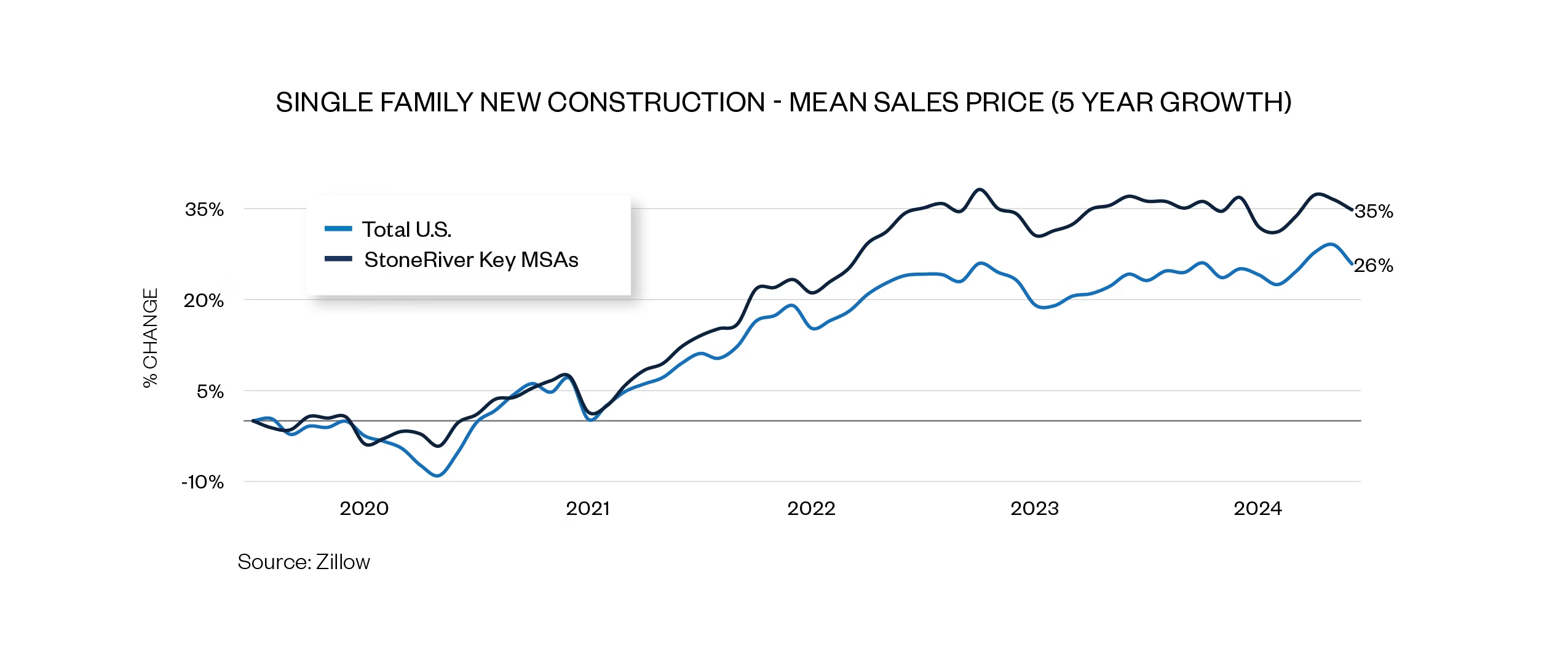

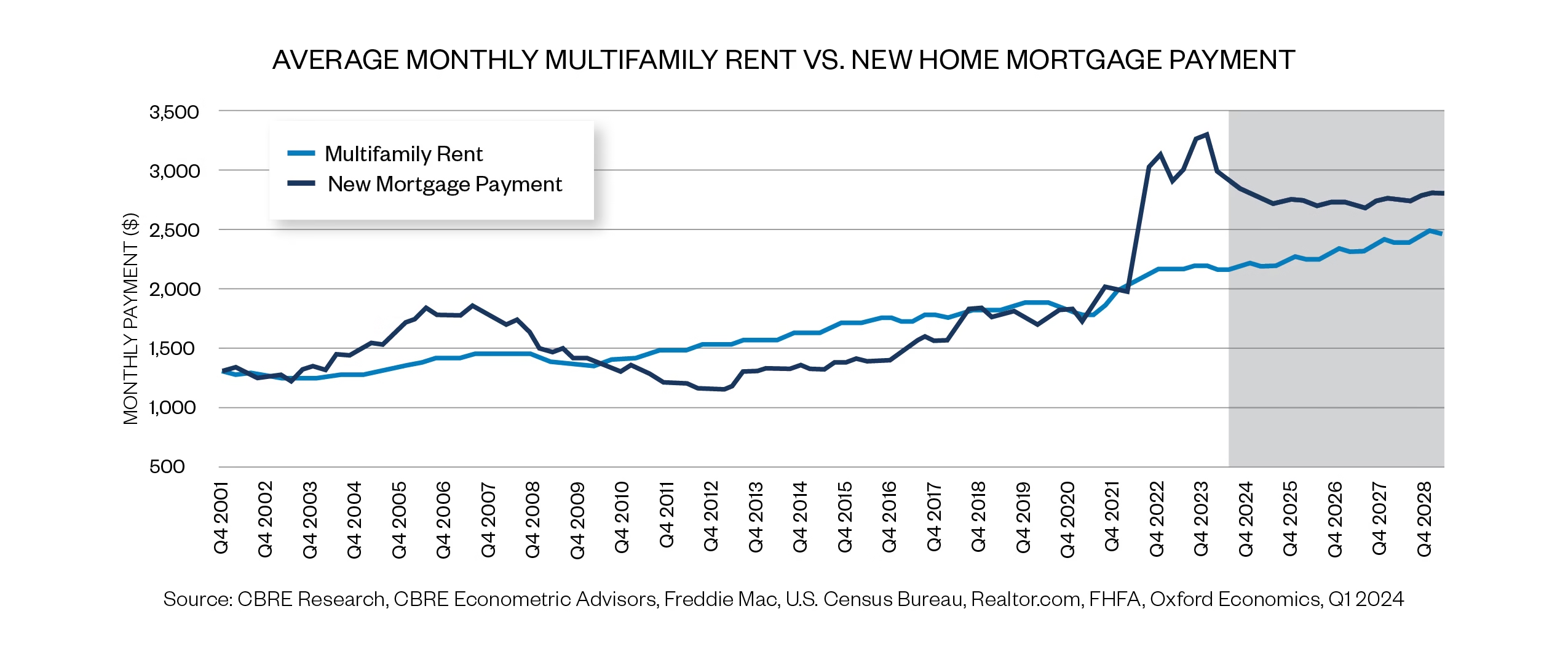

The rising cost of homeownership and the cost-saving advantages of apartment living also strengthen the demand for multifamily housing. Among the contributors to the rising costs of homeownership are mortgage interest rates and home prices. The average 30-year fixed-rate mortgage rate was 6.12% as of October 3, 2024, compared with 2.99% as of October 7, 2021. Additionally, the median sales price of a newly constructed home in StoneRiver’s Key MSAs increased 35% over the last five years, compared with a 26% increase nationwide. Due to these factors, the average monthly mortgage payment (not including insurance or other homeownership expenses) for a newly purchased home exceeds apartment rents by 38% and is projected to continue outpacing rents through at least 2028. Even if mortgage rates begin to fall, many homeowners who purchased or refinanced when interest rates were far lower a few years ago may be reluctant to sell their homes, constraining supply and placing upward pressure on prices. A recent working paper published by the Federal Housing Finance Agency estimates that this “lock-in” effect decreased the sales of homes with fixed-rate mortgages by 45% in Q2 2024, prevented 1.72 million home sales between Q2 2022 and Q2 2024, and increased home prices by 7.0%. Single-family construction has also slowed, further constraining supply and shifting demand to apartments.

Apartment housing also offers several other cost benefits for renters, such as lower utility costs, little or no maintenance expenses, access to amenities such as fitness centers and pools, no real estate taxes, flexibility to move (including to work remotely), and more affordable insurance premiums. Meanwhile, homeowners are often saddled with rising property taxes; soaring insurance premiums, utilities, and maintenance costs; upkeep and replacement of appliances; HOA or condo fees; landscaping expenses; the opportunity costs associated with illiquidity and saving for a down payment; and the time, hassle, and expense of selling the home when desired.

In addition to the costs of financing and maintaining a home, the elevated inflation beginning in 2021, growing levels of student debt, and tighter lending standards, among other factors, have made it increasingly difficult for would-be home buyers to save for an adequate down payment. These factors cause young adults to delay homeownership in favor of renting.

Occupancy and Absorption are Stabilizing in the Southeast, Indicating Healthy Demand

As we discussed in previous white papers, the multifamily sector, nationwide and in the Southeast, saw a surge in new supply beginning in 2020. However, the Southeast’s strong employment, its growing population of renters, the rising cost of homeownership, and the unique dynamics that limit single-family supply nationwide have maintained a healthy demand for apartments in the region.

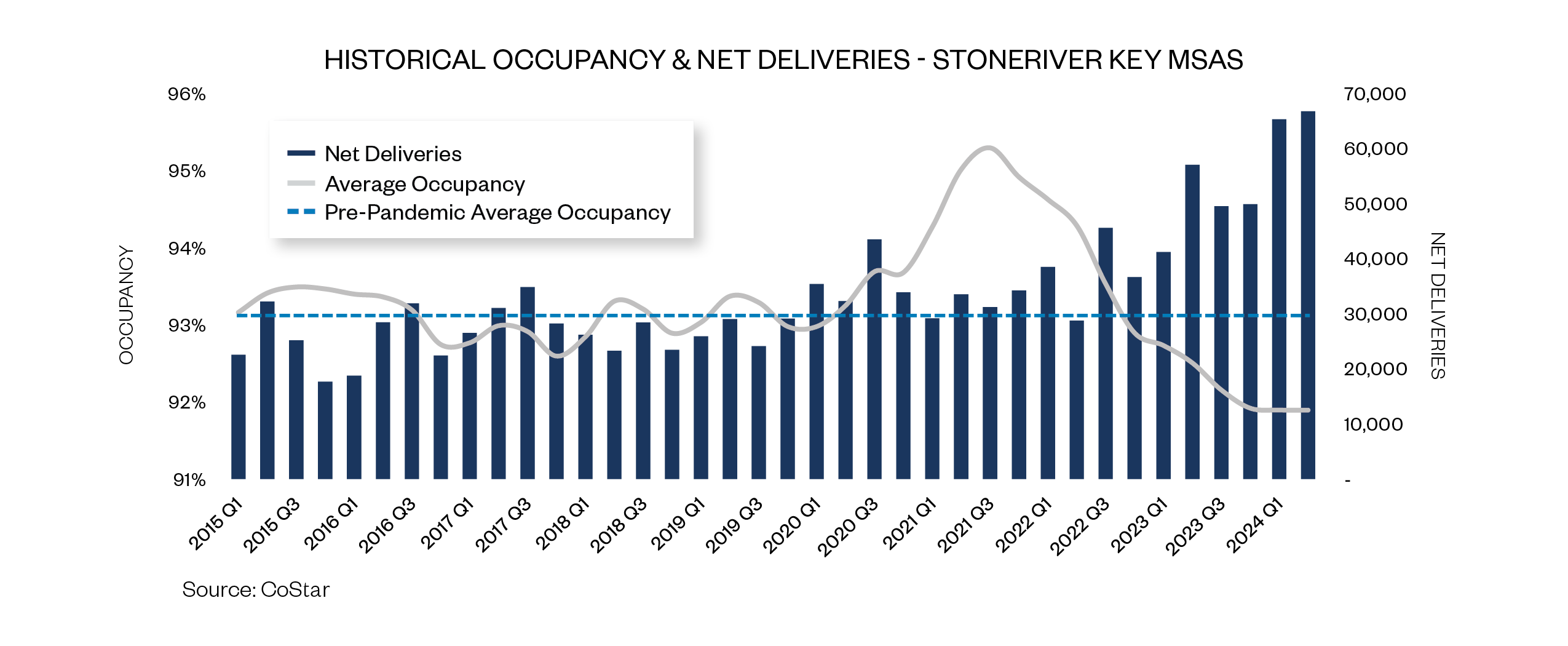

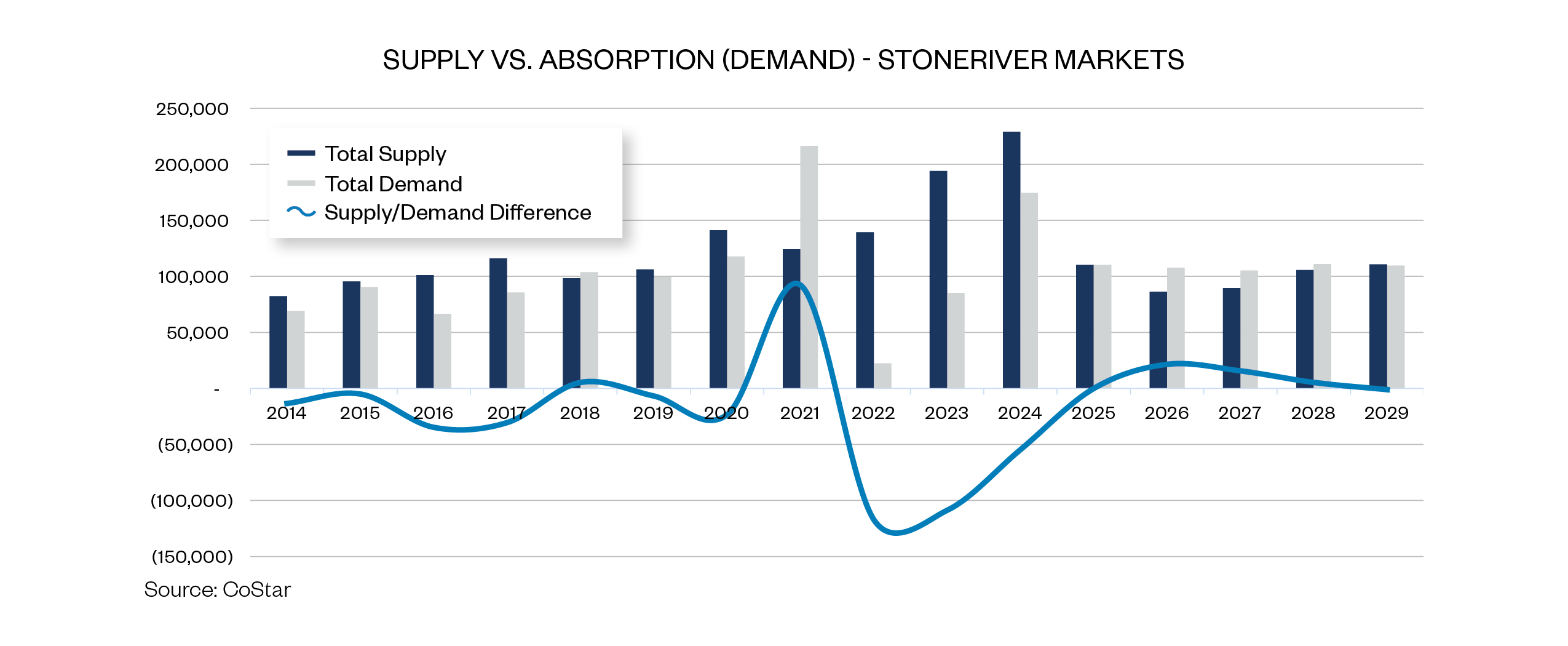

As new units entered the market, occupancy predictably dipped. However, occupancy is stabilizing; in our Key MSAs, average occupancy has remained at 91.9% for the last three quarters, just slightly below the national average of 94.0%. Additionally, projections indicate that absorption in our Key MSAs is improving and will reach an equilibrium compared to new supply by 2025. Both of these trends indicate healthy demand and favorable prospects for our Southeastern markets.

Conclusion

In conclusion, the Southeast exhibits thriving multifamily demand, driven by its robust job markets and rapid population growth among the younger renter population. Additionally, homeownership continues to be a cost-prohibitive or less attractive option for many. We believe that by aggressively sourcing, rigorously underwriting, and efficiently operating high-quality multifamily communities in select markets in the Southeast, StoneRiver can deliver superior risk-adjusted returns to its investors.